Carbon Capture and Storage (CCS) – Are We There Yet?Analyzing the target level of EUA prices to incentivize CCS adoption in Europe

By Oktay Kurbanov and Eron Bloomgarden

Introduction

In the discussions of carbon allowance future price trajectories, the cost of abatement technologies often comes up as a fundamental factor that may set a "ceiling" on European Union allowance (EUA) prices. In other words, if the carbon allowances reach the abatement cost levels, the companies will simply implement new abatement technologies and stop emitting CO2. The revenue from selling unused carbon allowances and/or savings from not buying them due to cleaner operations will cover the expenses. Along the same reasoning, to assess a potential upside of carbon allowance prices, the abatement cost for each of the major polluting sectors is compared to the carbon allowance price levels in the respective market. The recent rise of EUAs to €100 per ton levels brought the price of allowances higher than some lower-cost abatement technologies. Does it mean that EUA prices start facing headwinds due to abatement technologies?

While this logic is intuitive, the reality of implementing these technologies is a lot more nuanced than just comparing the two numbers. This paper focuses on carbon capture and storage (CCS) technology to illustrate this point and to show that the impact of CCS on EUA prices before 2030 is expected to be minimal:

- The target level of EUA prices to incentivize mass adoption of the CCS abatement technology in Europe is estimated to be €165, which is 80% higher than current EUA prices (around €90). [1] Numerous risk factors explain this high target level, and EUAs have a long way to go to reach it;

- European policies and regulations have to be further developed to ensure proper scaling of CCS transport and storage infrastructure, which will take time given the lengthy nature of the European legislative process;

- European CCS capacity targets for 2030 represent only 3-4% of the current emissions cap.[2] The projected 2030 annual capture of 70 metric tons (Mt) is also 26x more than the current operating volume, giving a sense of the major CCS scaling effort required to meet this goal.[3]

Risk factors

The high target EUA levels stated above are explained by key economic, logistical, and risk factors:

- CCS abatement costs are typically computed using an average cost over a 20-year project's life, combining both capital expenditures and operational costs ("Levelized Cost of Carbon Abatement"). This obscures very high financing needs to implement new technologies, which acts as a barrier to adoption at a mass scale.

- Successful implementation of CCS technologies is contingent on the price and availability of CO2 transport and storage. This will add meaningful costs to the abatement and, most importantly, require major planning, agreements, and regulations to be developed – a process that will take years to complete.

- Given high capital intensity, scaling CCS technologies will require attracting private capital. To offer attractive returns over the 20-year period and compensate investors for risk, carbon allowance prices must have a substantial "return premium" over abatement costs to achieve attractive levels of internal rate of return (IRR).[4]

- The net revenue from EUAs (either selling unused or not needing to buy due to cleaner operations) is a key determinant of the success of the project. However, the high annual volatility of EUA prices places this revenue at risk. Risk-averse financing entities will require an additional price-risk premium built into the observed levels of carbon allowances to be comfortable with project viability.

In what follows, the risk factors are discussed in greater detail.

Beyond CCS abatement costs: components of target EUA price to make projects attractive

Through using an example of a natural gas power plant, this paper analyses major cost components of the carbon capture technology implementation as well as additional factors determining EUA price levels required to make CCS projects financially attractive. We will see that EUA prices have to be significantly higher than abatement costs to incentivize undertaking these projects at scale and to secure the required funding.

Using data compiled by the National Petroleum Council (NPC), a 560 megawatts (MW) gas-based power plant will emit up to 1.5 metric tons of CO2 per year.[5] According to the NPC, building such a CCS facility will cost €613 million in capital investments. To commit to such a high investment, the funding entities will require a meaningful return. NPC assumes 12% IRR as a required return on investment, which is typical for projects of this nature.

The revenue from this project is assumed to come from selling unused carbon allowances or avoiding buying carbon allowances needed for compliance due to reduced emissions (such avoidance is treated as revenue for project planning purposes). Consequently, the price of the EUA allowance multiplied by the annual carbon capture amount represents the revenue from this project. The "required return premium" to meet 12% IRR is built into the target EUA price level, which is used to compute revenues. With these assumptions, Figure 1 demonstrates the cash flows from this project[6]:

Figure 1. Cash Flows from Installing a CCS Facility at a 560 MW Natural Gas Power Plant

Source: National Petroleum Council CCS facility data, CLIFI cash flow model

There are a few observations to make from the above graph. The capex[7] costs are very high, with a construction lead-time of 3 years before any revenue is generated. The cash payback period of this investment is 9 years (abstracting from time-value). To earn an attractive financial return of 12%, one needs to wait much longer, 23 years (lead time + project life). Finally, the simplified model in Figure 1 assumes the revenue remains at a flat, guaranteed level each year. However, with the high volatility of EUA prices, this revenue is anything but guaranteed. To ensure the target revenue levels are achieved with high certainty, the project's financial decision-makers must add an additional price risk premium into the target EUA price to be comfortable that even in an adverse price trajectory, the revenue from the project will be enough to meet stated IRR goals. This premium adds about 10% to the target EUA price.[8]

To come up with a single number representing an all-in cost of this project, all costs are averaged over the project life (20 years) – producing "levelized" cost numbers. Table 1 below shows the breakdown of the levelized cost of carbon abatement:

Table 1. 20-Year Levelized Costs for a CCS Facility at 560 MW Natural Gas Plant

One notices that the initial capital investment is just one of the few major components of the overall costs. The CCS project also has high energy costs to run the facility to power compressors, motors, pumps, and fans, as well as to generate steam to separate CO2 from the solvent where it is initially absorbed. There are also high non-energy costs to operate and maintain the equipment and to replace process chemicals. Finally, the CCS facility needs to pay for the transportation and storage of captured CO2, which is a significant cost component.

Table 2 below shows additional components of the target EUA price levels that make the project attractive to achieve an IRR of 12% (return premium)[9] and provide an additional cushion for price volatility (the price risk premium)

Table 2. Components of the Target EUA Price to Commit to the CCS Project

The table above illustrates that the abatement costs alone are poor predictors of the target EUA price levels required to induce commitment to CCS projects at a great scale. EUA prices need to rise substantially above the abatement costs to provide proper compensation for operational project risk (required return premium), as well as compensation for revenue risk (price risk premium).

The cost of carbon capture and storage in Europe

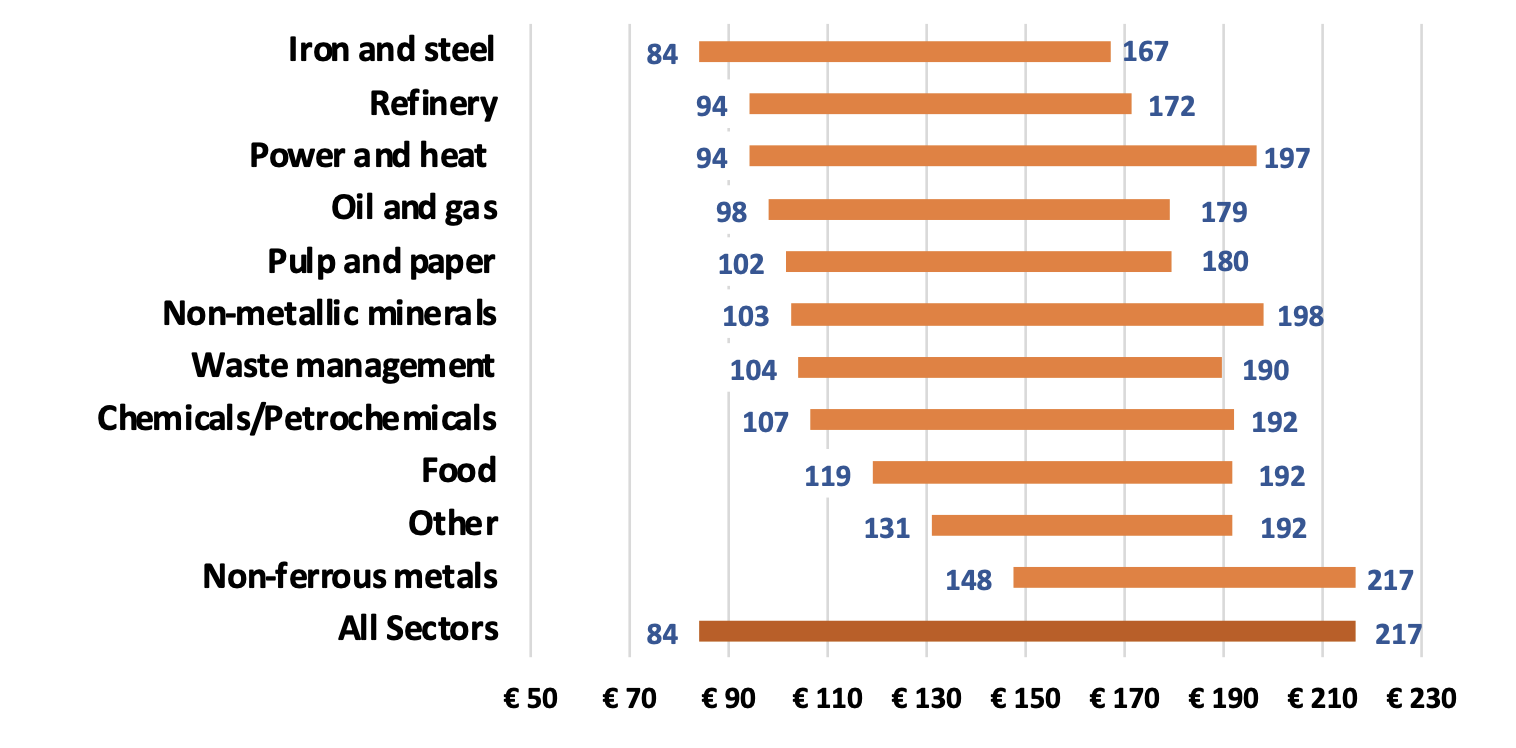

Figure 2 presents the summary of CCS implementation costs across European countries by analyzing capex and opex[10] costs, as well as transport and storage costs across different sectors and regions – following the 20-year levelized cost methodology discussed above.[11] Sector differences are driven largely by differences in CO2 concentrations in each sector and by the availability of process heat that can be utilized for the CO2 capture processes. Transport and storage costs will vary depending on the distance from the available pipelines, mode of transportation, and storage hub availability in the region. Note that these cost estimates also incorporate a 12% required rate of return – making these more comparable to the target EUA levels discussed above. The price risk premium is not included, which would add about 10% to these estimates:

Figure 2. Levelized CCS Costs in Europe

The summary above indicates that the target EUA price level for the vast number of CCS projects is still far above the current levels (around €90 per ton). [12] Looking at the average cost across all sectors and adding the 10% price risk premium produces €165 for the average target EUA level needed for a mass-scale CCS adoption for the majority of European sectors and regions. This target is 80% higher than current EUA prices, leaving considerable room for EUA appreciations to reach average critical targets to incentivize CCS transitions at scale.

An example of a recent CCS project illustrates the risk of cost overruns and the need to build in return and price risk premiums in project planning. On April 26th, 2023, it was reported that Norway halted its carbon capture project at the Klemestrud waste-to-energy facility after projections of cost overruns.[13] The initial project costs were estimated at around €479 million. The waste-to-energy facility emits 400,000 tCO2, with 90% of emissions projected to be captured. Using a 20-year project period and the same methodology as in the above analysis corresponds to a levelized cost of €222 per ton, even before adding required return and price risk premiums. This number by itself is outside of any reasonable range for CCS projects at waste-management facilities in Europe, as seen in Figure 2, pointing to the vested interests of the governments and regulatory bodies to see continuing EUA price appreciation to improve the feasibility of these projects.

Infrastructure and regulatory work

Even if economic hurdles were overcome, an emitting entity might remain hesitant to adopt capture technology if developments in infrastructure for two other parts of the value chain – transport and storage – do not occur at the pace needed, as we discuss below.

In fact, cross-border transport and storage of CO2 is an issue that is highly relevant in Europe. Many EU countries with high emissions do not have the required geological capacity for CO2 storage (be it onshore or offshore), where CO2 needs to be exported to countries with abundant storage capacities. Only recently, we started seeing bilateral agreements for transporting CO2 across European borders, such as Germany's and the Netherlands' agreement with Norway to transport and store CO2 in the Norwegian shelf of the North Sea.[14] However, a more comprehensive and streamlined set of regulations cross-Europe is needed to ensure streamlining of CCS project development.

One of the regulatory steps was taken by the European Commission through its Net-Zero Industrial Act (NZIA), where it set a target for CO2 storage on a continental level, 50 Mt per year by 2030.[15] This should provide higher investor confidence that CO2 captured in the CCS facilities they finance will have an eventual outlet. International Energy Agency (IEA) predicts that by 2030 around 70Mt CO2 will be captured in Europe per year.[16] However promising, these numbers represent a small part of the total volume of capturable CO2 in Europe, which stands at 1,260Mt per year. In terms of the potential impact on the ETS, these targets are only 3-4% of the current European emissions cap.[17] IEA's 2030's forecast is also 26x higher than the current CCS operating capacity in Europe, giving a sense of the effort required to meet this ambition.

Conclusion

Despite its technical maturity, CCS remains a solution that carries high capital and operational costs and is fraught with project risks, as well as uncertainties of the future revenue stream, given the high volatility of EUAs. Current EUA prices, despite testing €100 levels, are still insufficient to cover these complex costs. While there is a strong industry enthusiasm for CCS-based abatement and its role in achieving net zero targets, the financial hurdles and risk considerations discussed in this paper are slowing down the widespread adoption of CCS technologies. This is why CCS is unlikely to have any meaningful impact on EUA prices any time soon. Financial incentive mechanisms such as tax credits, grants, or carbon contracts for difference will help de-risk investments. However, the most direct and market-driven mechanism to encourage the deployment of CCS at a mass scale is strong policy support for the EU ETS and the continuing appreciation of EUAs to reach required target levels, as discussed in this paper. Based on current project economics and risk factors, EUAs have a long way to go.

[1] Source ICE data. Average price of Dec23 EUA futures from 1/1/2023 through 5/18/2023 was €90.20.

[2] European Commission (2023), Net-Zero Industry Act: Making the EU the home of clean technologies manufacturing and green jobs. Using a combined UK and EU ETS 2023 cap of 1659Mt.

[3] Source: IEA, “Carbon Capture, Utilisation and Storage”, Sep 2022, https://www.iea.org/reports/carbon-capture-utilisation-and-storage-2.

[4] Internal rate of return (IRR): calculates compounded rate of return on an investment given an expected future cash flow, excluding external factors, such as the risk-free rate, inflation, the cost of capital, or financial risk.

[5] National Petroleum Council, “Meeting the Dual Challenge, a Roadmap to At-Scale Deployment of Carbon Capture, Use and Storage”, Chapter 2, updated March 12, 2021 (“NPC report”).

[6] Using operating costs and other assumptions from the NPC report, CLIFI cash flow model.

[7] Capex: short for capital expenditure, a company or organization’s major, long-term expenses such as physical assets.

[8] Assuming 30% volatility, 23-year horizon and 95% confidence level under normal distribution.

[9] Not to be confused: to achieve 12% IRR, the premium must be much higher than the levelized abatement cost x 12% since its magnitude is driven by the initial capital expenditures outlay.

[10] Opex: short for operational expenditure, a company or organization’s ongoing, day-to-day expenses.

[11] Data sourced from Carbon Limits for Clean Air Task Force (2023). The cost of carbon capture and storage in Europe.

[12] Source ICE data. Average price of Dec23 EUA futures from 1/1/2023 through 5/18/2023 was €90.20.

[13] Reuters, “Carbon capture project in Norway temporarily halted by high costs”, April 26th, 2023.

[14] IEAGHG (2022). World’s first commercial pact on cross-border CO2 transport and storage.

[15] European Commission (2023). Net-Zero Industry Act: Making the EU the home of clean technologies manufacturing and green jobs.

[16] Source: IEA, “Carbon Capture, Utilisation and Storage”, Sep 2022, https://www.iea.org/reports/carbon-capture-utilisation-and-storage-2.

[17] Source: UK Government, European Commission. Using a combined UK and EU ETS 2023 cap of 1659Mt.