European Carbon in Transition: ETS1, ETS2, and the Investment Outlook

BY OKTAY KURBANOV, PARTNER AT CLIFI

Introduction

For a couple of years since the “Fit-for-55” reform package became a law, the European carbon market has been driven mostly by the economy and coal-to-gas switching, as the regulatory activity slowed down. We are now entering a phase where regulatory developments are accelerating, many of which have the potential to tighten the supply-demand balance and, as a result, provide tailwinds for European Union carbon allowances (EUAs):

- New Sectors Added to CBAM

Legislative review of Carbon Border Adjustment Mechanism (CBAM) in the second half of 2025 has a strong possibility of expanding its scope to additional sectors as well as the downstream supply chain. CBAM serves as a carbon tariff on imports for select high-emitting products into the EU. This expansion could drive up hedging demand from importers into the EU, increasing the demand for carbon allowances.

- Inclusion of International Aviation

The CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) assessment by the European Commission in 2026 may result in extending the coverage of the EU Emissions Trading System (ETS) to include international aviation. Should this occur, there will be additional traded demand entering the European carbon market.

- REPowerEU Receeding

The tail phase of REPowerEU starting in 2027, where auction supply will be reduced to compensate for extra allowances auctioned in 2023-2026. 57Mt of allowances are expected to be withheld from auctions each year from 2027 through 2030, reducing supply by 6%.

There is also another significant event on the horizon: the launch of the second European Union ETS (“EU ETS2”) covering buildings, transport, and small industry. The upcoming launch of the EU ETS2 has major implications for carbon investors:

- Comparable Investment Opportunity

It represents a compelling investment opportunity at a scale comparable to the current EU ETS (“EU ETS1”). At its launch in 2027, ETS2 emissions will be capped at 1.04BMt, which is similar in size to the ETS1 cap of 1.12BMt in that year. Both ICE and EEX have launched EUA2 futures products to facilitate secondary market trading ahead of ETS2’s operational start.

- Tighter Allowance Cap

As ETS2 evolves from its early launch stage to a tighter cap, it could support strong upward price pressure for EUA2s due to the expected tight supply-demand balance of the program.

- Market Interaction Drives Demand

ETS2 will likely indirectly interact with ETS1 by spurring power demand due to the electrification of transport and building heating. This should, in turn, drive up power emissions in ETS1 due to the fossil-based power-generation component, adding demand pressure on EUAs.

EU ETS1: Things Are About to Get More Interesting

One of the most impactful events in the global carbon markets will be the arrival of CBAM, which enters its official compliance phase in 2026.[1] Despite the gradual phase-in, its immediate impact will be significant, driving hedging demand by exporters into the EU.[2] Prior to that, in the second quarter of 2025, the European Commission is set to deliver a legislative proposal to address key operational aspects of CBAM. One proposal will consider exempting EU exporting companies from EU ETS obligations to ensure their competitiveness in the global markets. Another will address the circumvention issue where non-EU companies carve out the clean part of their production to export to the EU, while not decreasing their carbon intensity overall. Finally, the Commission will review the possibility of extending the scope of CBAM to other sectors and downstream products. Addressing circumvention and scope expansion is welcome news to strengthen CBAM and potentially drive incremental hedging demand for carbon allowances.

Up until now, the aviation sector was a relatively small part of the EU ETS1, limited to flights within the European Economic Area (EEA). In 2024, it contributed 5.4% of emissions to the covered sectors in ETS1.[3] The scope of aviation emissions coverage could increase dramatically in 2026, when the European Commission conducts its assessment of the effectiveness of CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) to deliver the goals of the Paris Agreement.[4] For context, CORSIA a global market-based program developed by the International Civil Aviation Organization (ICAO) to cap net emissions from international flights at 2020 levels by requiring airlines to offset emissions above that baseline. If deemed ineffective, flights departing the EEA will become covered from 2027 onward. If revised, will add incremental demand of 80Mt for carbon allowances,[5] increasing the projected 2027 emissions by 4%.

As it stands now, CORSIA’s effectiveness is at risk. It has faced challenges in securing a sufficient supply of eligible offsets to satisfy aviation demand. For example, the vast majority of credits eligible for Phase I (2024-2026) have not been issued and they have a significant risk of supply failure due to an insufficient regulatory framework to ensure corresponding adjustments in host countries.[6] There are also indications that Trump’s administration could abandon CORSIA, especially after having already exited the Paris Agreement, which will drastically decrease its coverage and thus effectiveness of CORSIA.[7] Consequently, the chances of the EU ETS1 scope expansion to include international flights are significant, pushing the range of possible “high-emissions-demand” scenarios upward.

Another major supply-side event will start unfolding in the 2027-2030 period with the conclusion of REPowerEU funding. The initiative was introduced in May 2022 to finance European initiatives, diversify energy supplies, and accelerate renewable energy capacity.[8] The EU ETS1 provided €20 billion of financing for REPowerEU by bringing forward the supply of auction allowances from future years and using their proceeds for the program. These sales result in an extra supply of allowances during 2023-2026, which has had a considerable dampening effect on EUA prices. In order to keep the total emissions budget neutral, ETS1 will reduce auction supply in 2027-2030 by 230Mt (57Mt each year), which represents 6% of total supply during that period. Given the extra supply has weighed heavily on EUAs, one can expect a reverse market reaction, i.e., upward price pressure, to the shrinking supply of allowances starting from 2027. This future dynamic has been captured in analysts’ forecasts, with the period around 2027 expected to become a crunch-point in the EUA market, with the annual demand outstripping supply by around 200Mt, or 18% of the total annual emissions budget.[9] This imbalance should support strong price momentum, as illustrated inthe chart below:

Figure 1. EUA Price Forecast

Source: ICIS, CLIFI

The following sections discuss the EU ETS2, its supply-demand outlook, and its interaction with ETS1.

EU ETS2: The Younger Sibling is Just as Ambitious

The EU ETS (ETS1), first introduced in 2005, currently covers about 40% of the region’s emissions, including sectors such as power, industry, maritime, and aviation.[10] As part of its “Fit for 55” initiative, the European Commission introduced a new emission trading system, “ETS2”, to cover emissions from fuel combustion in buildings, transport, and small industry not covered by ETS1. The Commission found emission reductions in these sectors insufficient to meet the 2050 climate neutrality goal; therefore, the ETS2 was created to complement the European Green Deal policy and to create market incentives for investments in innovations and electrification in the building and transport sectors.[11] Combined, ETS1 and ETS2 will cover about 75% of the EU’s emissions.[12] Introduction of ETS2 opens a great investment opportunity for a few reasons:

1. Market size. Upon its launch in 2027, ETS2 will become the second-largest carbon market in the world, open to global financial investors. Its 2027 emissions cap is set to 1043Mt vs. the ETS1 cap of 1120Mt for the same year. The international exchange ICE has already launched an ETS2 carbon allowance futures contract, “EUA2,” while the European Energy Exchange (EEX) will launch EUA2 futures in July 2025. Based on the current indicative prices for EUA2, the secondary futures market for ETS2 is expected to be over $600 billion in annual trading volume following the launch of auctions in 2027.[13] This new ETS2 is welcome news for carbon investors looking to invest in new investable markets at scale.

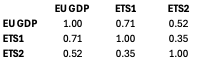

2. Diversification. It could also offer diversification[14] value vs. EUAs. Since EUA2s cover different sectors, they are driven by different supply-demand dynamics and different dependency on the economic cycle. It is important to note that the demand for building heating is non-cyclical. Moreover, the small industries sector also shows a much weaker relationship to the economic cycle. This make demand for ETS2 emission allowances less dependent on the economic cycle vs. ETS1, which is power and energy focused, both of which are more driven by industrial demand. Table 1 illustrates this point by showing the correlation of ETS1 and ETS2 emissions to the EU GDP as well as to each other:

Table 1. Correlations of ETS1, ETS2 annual emissions vs. real GDP (2005-2024)

Source: CLIFI

Compared to ETS1, ETS2 emissions show lower correlation to GDP of 0.5 vs. 0.7. Their correlation to ETS1 emissions is positive but not notably high, around 0.4. As demand for emission allowances is closely related to price performance, low correlation in emissions demand vs. ETS1 and vs. GDP makes it reasonable to expect that EUA2 can offer price performance diversification[15] in global portfolios.

3. Tight Supply-Demand Balance. Off the start, the ETS2 is expected to have a tight supply-demand balance, supportive of strong potential for price appreciation. To relieve initial pressures of new sectors adapting to carbon pricing, the European Commission front-loaded supply by auctioning 30% more of the annual emissions budget in the first two years, which is then offset by a reduction of the auction supply in years 2029-2031. This front-loading results in initial annual surpluses in the first two years, followed by annual deficits in the subsequent three years. This dynamic is reflected in the supply-demand projections shown in Figure 2:

Figure 2. ETS2 Supply / Demand Balance of Allowances

Source: CLIFI

Based on these projections, ETS2 will be in a very tightly balanced state starting from 2030-2031. A key strategy for achieving this balance is the implementation of abatement technologies, which reduce or remove pollution from industrial or energy processes such as fleet electrification, heat pumps, electric boilers, electric and hydrogen heaters for small industry, among other measures. The marginal abatement cost curve (MACC) illustrates this concept by showing the cost of reducing one additional unit of emissions using different abatement options, ranked from cheapest to most expensive. It helps identify the most cost-effective ways to cut emissions. The majority of these technologies become economically feasible only at sufficiently high EUA2 prices, as one can see in Figure 2:

Figure 3. ETS2 Marginal Abatement Cost Curve

Source: ICIS, excluding subsidies, 2025 costs

The tight supply-demand balance and costly abatement technologies are expected to contribute to upward price pressure for EUA2 carbon allowances as illustrated in the chart below:

Figure 4. EUA2 Price Forecast

Source: ICIS

Considering expected extra supply early on in the lifecycle of ETS2, we believe investors have a chance to enter the market at accessible price levels to capitalize on the future expected appreciation, where EUA2 prices can reach levels above €200 by 2030 according to Independent Commodity Intellegence Services (ICIS).

ETS1 & ETS2 Power Struggle: Electricity Demand

While ETS2 will operate separately from ETS1, it will produce incremental demand for electricity, which is covered by ETS1. This demand will be driven by the abatement technologies previously mentioned. The chart below illustrates the incremental energy demand by various abatement areas:

Figure 5. Power demand from abatement in ETS2

Source: ICIS

By the year 2030, this incremental demand is expected to rise to 400TWh. For comparison, in 2024, the European Union generated about 2700TWh of electric power,[16] which makes this an incremental 15% increase in power consumption. While the EU actively pursues renewable energy sources, it will retain fossil-based power generation in the next decade to supply its baseload power. Assuming that REPowerEU’s ambitious goal of 69% of renewables by 2030 is achieved (up from 43% in 2024), it will still leave at least a 10% gap to be filled by coal and gas.[17] This will result in 30Mt of additional carbon emissions, which will increase demand for ETS1 carbon allowances by about 3%.[18] Considering a tight supply-demand balance of ETS1 by the end of the decade, this should provide a meaningful price support for EUAs.

Conclusion

European carbon is entering into a very dynamic phase given the concurrence of events unfolding that are expected to provide favorable supply-demand dynamics. The CBAM compliance phase starts in 2026, with a possibility of an expanded scope. There is a potential aviation inclusion post-CORSIA review in 2026. Finally, the REPowerEU-related auction volume reduction will start in 2027 and continue through 2030. The ETS2 is set to be launched in 2027, offering an additional investment opportunity of similar scale and scope. It is also likely to add incremental demand for EUAs due to increased power demand from building and transport electrification. While these trends are 1-3 years out, we believe EUAs are expected to start pricing-in these upcoming dynamics in advance.

[1] European Commission, Carbon Border Adjustment Mechanism, 3/8/2025

[2] See CBAM and Carbon Diplomacy: Catalyst for Carbon Markets, Oktay Kurbanov, 10/8/2024

[3] Source: CLIFI

[4] European Commission, Reducing Emissions from Aviation, accessed 6/10/2025

[5] Source: Clear Blue Markets

[6] AlliedOffset, illuminem, CORSIA: Market developments and forecast scenarios, 5/30/2025

[7] Fastmarkets, US withdrawal from Paris Agreement raises questions over CORSIA credit supply and demand, 1/23/2025

[8] European Commission, REPowerEU: Affordable, secure and sustainable energy for Europe, accessed 6/12/2025

[9] Source: CLIFI

[10] ICAP, EU Emissions Trading System for buildings and road transport ("EU ETS 2"), accessed 6/17/2025

[11] European Commission, ETS2: buildings, road transport and additional sectors, accessed 6/17/2025

[12] Carbon Market Watch, FAQ: What is the EU Emissions Trading System (EU ETS), 2/29/2024

[13] Source: CLIFI. Assuming convergence of ETS2 to the same ratio of secondary vs. primary market size.

[14] Diversification …

[15] Id.

[16] EMBER, 2024 at a glance, accessed 6/19/2025

[17] European Commission, Implementing the Repower EU Action Plan, 5/18/2022. Assuming nuclear generation continues to provide ~20% of the total electricity.

[18] Source: CLIFI